I am often asked: “When will the next economic crisis happen, what will cause it, and what can average workers do about it?”

Fair questions to ask. Imagine you are on a tall mountain and it has been snowing heavily. You see the swollen snowbank. You do not know when it will burst. You cannot know which snowflake will set it off. But you do know that eventually it will scream down the mountain, wreaking havoc.

Even leading economic commentators sometimes hesitate to call it, when the situation is so bad. There is always the risk of setting off a panic. Appearances are everything and volatile currencies, simultaneous property and stock market bubbles, all with people exploiting historically low interest rates with their historically high debt levels, make for a dangerous recipe indeed.

The governments and central banks responsible for the policies which caused these conditions have a fatal conceit. They have failed to heed the lessons of structural causes from the 2008 crash. Central banks meddling with interest rates have distorted our economy, causing huge misallocations of investment by stoking ‘the business cycle’ of boom and bust. This is compounded by governments’ ‘moral hazard’ cultivating policies of corporate welfare, insuring private banks to gamble wildly, which has led us to this situation, again.

Our governments are in denial and have simply doubled down on the very policies which have led us to this danger. For example: the bad banks of 2008 are still with us, they are now bigger, with even worse percentages of banking assets and derivatives. Everything that was bad in 2008 is worse in 2016.

To re-inflate property and stock market bubbles (to keep the party going), means government central banks have had to print money and suppress interest rates. This long running sham, since 2009, has distorted our economies to become addicted to cheap money and to debt. It has also destroyed incentives for workers to save. Thrift has been made a sin. A culture of short-termism, borrowing, spending and risky investment rules.

Cheap money is borrowed to flood the housing market, which combined with help-to-buy schemes and daft planning laws choking supply, has forced up property prices. The enormous property bubble has been re-inflated, again. The result can only be a terrible pop!

Also see: Latest dollar and pound exchange rates

Similar is true in the stock market. Cheap money is chasing yield and so flocks to stocks, driving up share prices, even if the economics of a company do not merit its share price.

As for the pound sterling, the purchasing power of this continually debased currency was already falling before Brexit. The uncertainty of looming Brexit negotiations has contributed to the pound’s fall against foreign currencies misperceived as being more stable. Sending money to Australia or traveling on the pound is increasingly expensive. It buys less and less.

Also read: Brexit four months on: UK is single and looking good

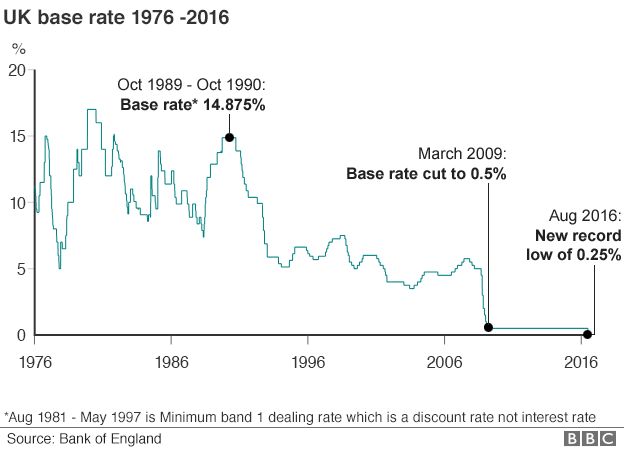

With soaring household and government debt, overleveraged banks, our cheap credit fuelled party cannot last forever. We will have to sober up. For an economy being so drunk on cheap money for so long, its hangover will be biblical. People, businesses, and governments can barely afford today’s absurdly low interest rates. Memories are short and people can scarcely remember base rates of 7%, 10% or 17%! When interest rates return to normality anyone overly exposed and unable to repay will be ‘up the creek.’ That will be a lot of people, businesses and governments.

Take your pick. The world economy is fragile; a house of cards. It could be a bank failure, a non-delivery of physical gold, another Chinese credit crunch, a geopolitical crisis; Russia, USA and the EU squabbling over a stray jet, for example. The possibilities are endless and the crunch catalyst may appear where it is least expected. These are known as a black swan events: impossible to predict yet have catastrophic ramifications.

In short, take control of yourself. Invest prudently, including in yourself. Seek historically sound investments for troubled times and become economically literate.

Historically, gold and silver will protect you in an economic crisis. Allocating a portion of your savings to physical precious metals is wise. Anyone can do this. Preferably store it in a foreign jurisdiction in a vault, outside the banking system. Governments like to tax and declare bank holidays during economic crisis (ask Europeans).

Gold or silver coins enjoy intrinsic value. Their purchasing power can soar during economic strife and they belong solely to you. You can buy silver coins for as little as £15. Allocating some of your savings to purchasing regularly, say, every couple of months will see you amass a nice discreet foreign investment portfolio of precious metals.

Of the foreign jurisdictions most attractive to invest in, one cannot surpass Singapore: a beacon of economic freedom and privacy. To this end, I spoke with Singapore based Gregor Gregersen Founder and CEO and Vergel Villasoto Director of Silver Bullion Singapore Pte Ltd: a bullion retailer and private storage vault. Gregor explained their customers increasingly include:

“Americans, British and Australians looking to take advantage of Singapore’s political stability, impressive privacy laws, low tax, safe foreign jurisdiction for those who seek to discreetly store some of their wealth outside their banking system.”

Silver Bullion’s growth is symptomatic of the distorted economic world we live in. People are increasingly catching on that the world’s debt addicted economies are unsustainable, swamped with risk and overdue for a major correction. The safest store of wealth is where it always has been during unstable times: physical gold and silver. Once enough people come to this epiphany, once enough confidence in the current charade evaporates, their game will be up. When that happens you will be thankful for your precious metal portfolio.

Investing in yourself is wise and becoming economically literate is not as hard as some might imagine. An easy introduction to economics is Henry Hazlitt’s ‘Economics in One Lesson,’ an enjoyable read which will enable you to understand and see through the smoke and mirrors in the media. A slightly more advanced book is Jim Rickard’s ‘The Death of Money.’ Both are acclaimed authors who will stand you in good stead.

We do face troubled times. The snowline is bulging, swollen by years of money printing and low interest rates fuelling huge credit binges. The avalanche is inevitable. Fortunately, there is still time to get your house in order and position yourself to prosper. Use it.

{kind=link}