Photo by Samuel Regan-Asante on Unsplash

Richard Bruce, University of Sheffield

The recent statement by David Cameron, the former UK prime minister, about his role as a lobbyist and adviser to insolvent finance company Greensill Capital has caused shock waves in business and government circles since it confirmed that the company was already in financial difficulties at the time of his activities.

But one major question getting less attention concerns the future of supply chain finance (SCF), an important tool in the financial arrangements between suppliers and their customers. Greensill was closely associated with this financing and has potentially rendered it unviable.

So what is supply chain finance and why should we be concerned?

In the early 2000s I worked as an external adviser to one of the big four accountancy firms on a brief from a well-known global consumer goods company that wished to increase its profitability. Part of the work was about enhancing the company’s cashflow.

Any business concerned about its cashflow has to look at three important measures. How long does it take to get money in from customers; how quickly are suppliers paid; and what level of stock needs to be held.

Increasing the time taken to pay suppliers would have been an easy and immediate way of increasing cash availability. But the proposed shift from settling invoices in 30 days to making it 90 days would have really annoyed suppliers.

A solution was found through discussions with the company’s bankers that helped develop what was initially called reverse factoring. As it became more widely adopted, it became known as SCF.

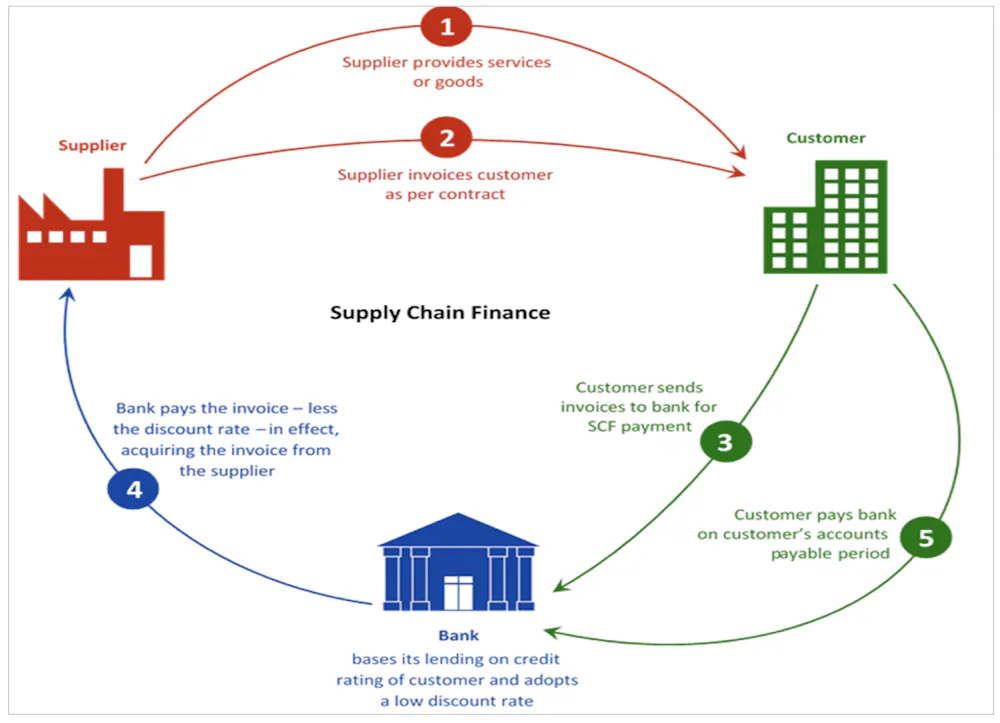

SCF essentially works by getting a bank to pay a customer’s invoice from its suppliers early, for a fee, so that suppliers can improve their cashflow. You can see this in the graphic below – click to make it bigger.

How supply chain finance works

In the case in which I was involved, SCF enabled our customer to move to new terms in which invoices were settled in 90 days. The suppliers were able to receive a substantial proportion of the payment due, typically 95% to 98%, when they required it, which could be on the original 30 days, or even earlier.

The customer’s excellent credit rating meant that the bankers could offer this financing at a fraction of the rate that the suppliers, with their less impressive ratings, could obtain through the existing system of invoice discounting, in which they borrowed from a bank or finance company to be “paid early”.

On the face of it, SCF was therefore a win-win for everyone: the customer holds on to their accounts payable for longer; the customer’s bank gains some new low-risk business; and the supplier can get paid a lot earlier at minimal cost. Obviously the supplier would prefer to be paid earlier without such financing, but they are often at the mercy of customers and this was the next best option. For many customers with excellent credit ratings, SCF quickly became the norm.

As it grew in popularity, variations were inevitably introduced. Some customers started to further extend payment terms, in some cases up to two-thirds of a year, relying on SCF to avoid real distress to their suppliers. However, even the very low discount rates offered to suppliers mount up to a significant reduction in the invoice settlement if payment is delayed for an extended period.

Greensill Capital was founded in 2011 and started encouraging the UK government to adopt SCF for procurement contracts. The customer in this case was the government, so banks could have virtually absolute security that their money was safe if they advanced payments to suppliers, meaning even lower interest rates for this SCF than that enjoyed by blue-chip private sector customers.

SCF soon became the norm for the payment arrangements for many suppliers to government. However, Greensill provided a twist in that the advanced payments to suppliers came from a bank within the Greensill group – Greensill Bank, based in Bremen, Germany.

Greensill also packed the invoices into a form of corporate bonds and offered these for sale. This relied on a system in which buyers took out credit insurance to protect them from customer defaults, but it ran into trouble when this insurance lapsed and was not renewed.

Credit insurance assessments are based on risk and the withdrawal of cover usually indicates a fundamental issue with the company. One of the investors who had acquired the bonds, Credit Suisse, reacted to this lapse in cover at the beginning of March 2021 by freezing its involvement, exposing itself to some US$10 billion (£7.3 billion) in potential losses as a result. This move led, in part, to Greensill being placed into administration a few days later.

Invoices forming part of the bonds would appear in Greensill’s ledgers as accounts payable whereas, it is being argued, they should be more correctly described as debt. The FT remarked that this procedure “can be used to mask spiralling de facto corporate borrowing”. There is talk of possible changes to accountancy practices that could remove the advantages in SCF from a supplier’s point of view by forcing them to acknowledge higher levels of debt on their balance sheets.

The danger here is that customers who use the more conventional SCF – working with their merchant or retail banks and offering suppliers a choice of the source of finance – may become tarred with the Greensill brush.

In an ideal world, suppliers would be paid on time by fair-minded customers. But pressures on prices through intense competition, partly a result of globalisation of supply chains, mean that many financially secure customer-companies see SCF, handled responsibly, as going a long way to satisfying their needs and – to a large extent – the needs of their suppliers.

Accounting practices may need to change to deter or outlaw the tactics used by Greensill, but it would be very damaging if SCF were abandoned entirely.

Richard Bruce, Lecturer in Global Supply Chain Management Accounting, University of Sheffield

This article is republished from The Conversation under a Creative Commons license. Read the original article.

{kind=link}

{kind=link}